Don't Fight The FED, The Great Portfolio Reset

"Don't Fight the FED"

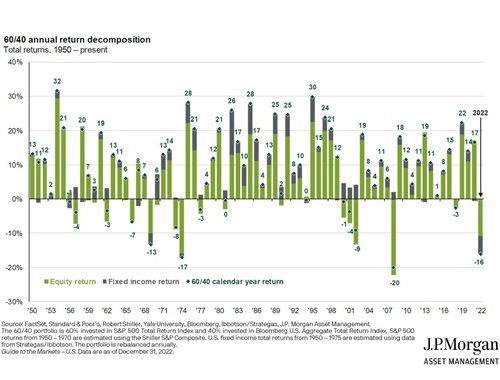

Don’t fight the Fed is probably a phrase that you have heard many times over the years. What it generally means is when the Federal Reserve is lowering interest rates, it is normally a good time to be buying risk assets as they become worth more in lower interest rate environments. What we found out in 2022 is that this effect also works in reverse. If the Fed is raising rates, especially at the speed that they did as we realized in hindsight, it is a good time to reduce your positions in risk assets.

As it turned out, the pace of rate hikes was the most rapid in modern times. With yields starting so low (0%-0.25%) and the rate of change in tightening so fast, nearly every segment of the fixed income markets experienced declines, especially bonds with long durations. The 10-Year Treasury note experience its worst year as measured by total return in over 200 years with a loss for the year of 16.33%, high grade corporate bonds declined 15.8% and the 30-Year Treasury bond lost 33.3% for the year.

In past periods of sharply rising interest rates, bonds have usually delivered positive returns since the income from a bonds coupon offsets the decline in price. However, during 2022, with very little coupon income, returns were historically weak.

In addition to the returns in the bond market, the returns in the stock market left much to be desired as domestic stock indexes such as the S&P 500 dropped 18.1%, the Russell Mid-Cap index declined 17.3% and the Russell 2000 fell 20.4%. Non-U.S. stocks weren’t much better with emerging market equities dropping 20.1% and The MSCI EAFE (Developed Markets Index) declined 14.5% as the end of year decline in the U.S. dollar propped up European and other markets such as Japan.